This shift is not just about convenience. It represents a fundamentally different philosophy about what a bank should be — one that is built around the customer’s actual behavior, spending patterns, and financial goals rather than around the operational constraints of a branch network. At the heart of this transformation is the rise of digital banking platforms that combine savings, credit, rewards, and payments into a single, seamlessly integrated experience.

For a large portion of India’s working-age population — particularly younger professionals, gig economy workers, and first-time earners — traditional banking has always felt slightly misaligned with how they actually live and spend.

Credit cards from established banks have historically required applicants to meet strict eligibility criteria: a minimum income threshold, a stable salaried position, an existing credit history. For someone just starting their career, or someone whose income arrives irregularly through freelance or contract work, these requirements effectively locked them out of credit entirely. The irony is that these are precisely the people who most benefit from access to a manageable credit facility — not to borrow recklessly, but to smooth out the natural cash flow variations that come with early-career financial life.

Savings accounts at traditional banks, meanwhile, offer minimal returns, buried under fees, minimum balance requirements, and customer service experiences that have not kept pace with the digital expectations of a generation that grew up with instant everything.

The gap between what young Indians need from their financial institutions and what those institutions have traditionally offered is what modern digital banking platforms have moved decisively to fill.

One of the most significant innovations in India’s evolving fintech landscape is the rethinking of how credit works for the individual consumer. Rather than treating credit as a product issued to a customer and then largely forgotten until the bill arrives, modern platforms are building credit facilities that are transparent, flexible, and genuinely designed to benefit the user rather than simply the lender.

The application process for financial products has traditionally been one of the most friction-heavy experiences a consumer can go through — lengthy forms, document submissions, waiting periods measured in days or weeks, and uncertainty about the outcome throughout. Modern digital platforms have compressed this timeline dramatically.

Registration and credit assessment can now be completed in a matter of minutes through a mobile app, with an instant decision provided at the end of the process. This is not just a convenience improvement — it represents a genuine change in who can access credit and when, making the system more responsive to real human needs.

One of the features that distinguishes thoughtfully designed credit products from predatory ones is the interest-free period — the window of time during which spending on credit incurs no interest charge, provided the balance is repaid in full by the due date.

When this feature is designed well and communicated clearly, it allows consumers to manage short-term cash flow gaps without paying a premium for the privilege. An interest-free period of up to 62 days, for instance, gives a user spending in early May until late June to repay their balance without any interest accruing — effectively functioning as a short-term, zero-cost financial bridge that supports responsible spending rather than discouraging it.

One of the most frustrating catch-22 situations in personal finance is the credit history problem: you cannot get credit without a credit history, but you cannot build a credit history without access to credit. For millions of first-time borrowers in India, this circular logic has been a genuine barrier.

Thoughtfully structured starter credit limits address this directly. By offering a smaller initial credit facility to users who do not yet have an established credit history, and then expanding that limit as responsible usage is demonstrated over time, these products create a genuine on-ramp into the formal credit system rather than a wall. Every on-time repayment builds credibility. Every billing cycle completed without default is a step toward a stronger credit profile and access to larger facilities in the future.

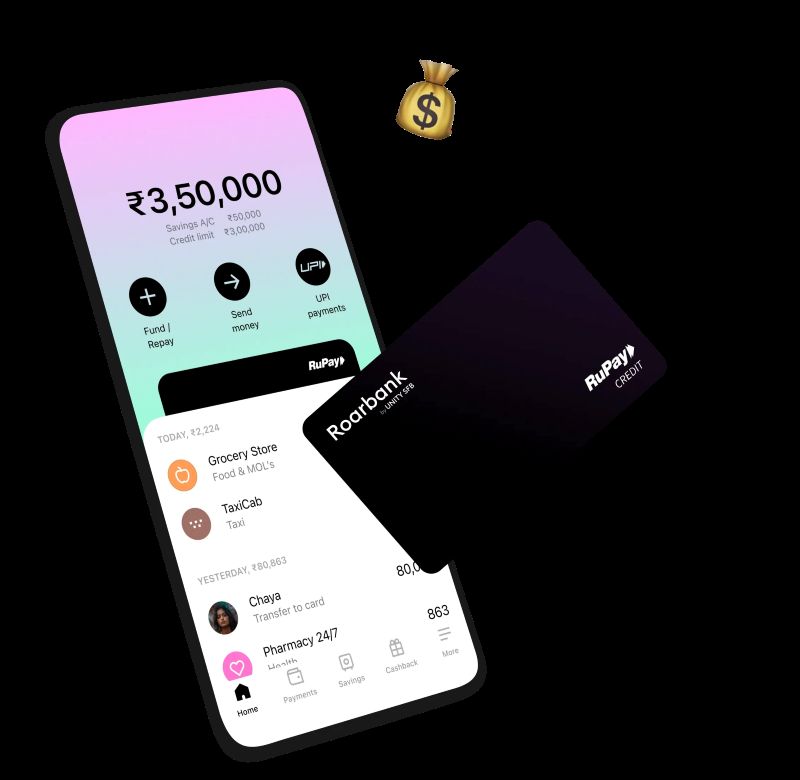

One of the most genuinely innovative structural features in modern digital banking is the integration of savings and credit into a single unified product — a single card, a single balance view, and a single interface managing both.

The practical mechanics of this model are straightforward but powerful. A user holds both a savings balance and an available credit limit within the same account. When they make a transaction, the system first draws from available savings funds. Only once those funds are exhausted does the credit facility activate, and only up to the approved credit limit.

This sequencing means the user naturally preserves their credit limit for situations where their savings balance is insufficient, rather than spending on credit unnecessarily. It also means that when funds are received — a salary payment, a freelance invoice, a family transfer — those funds immediately replenish the savings balance and restore the credit limit, keeping the user’s financial position clean and current.

The addition of cashback rewards on transactions made from both savings and credit balances means that everyday spending actively generates value for the user — whether they are spending their own money or utilizing their credit facility responsibly.

India’s Unified Payments Interface has fundamentally changed how the country transacts. UPI-enabled payments are fast, free, and universally accepted across an enormous and still-growing network of merchants, vendors, and individuals. For a credit product to be genuinely useful in the Indian context in 2026, UPI compatibility is not a nice-to-have — it is a baseline requirement.

Platforms that enable their credit limit to be used through UPI give their users access to the full breadth of India’s digital payment infrastructure without requiring them to carry or present a physical card. This matters enormously in a country where a huge proportion of everyday commerce — from street food vendors to neighborhood grocery stores to transport apps — runs through UPI rather than card terminals.

The best financial products are those that actively help users make good decisions rather than those designed to profit from bad ones. A well-designed digital banking platform should make it easy to track spending, monitor available credit, understand exactly when payments are due, and receive proactive notifications before issues arise.

Transparency in fee structures matters equally. Understanding the interest rate applicable after the interest-free period, the mechanics of the minimum amount due, and the consequences of late payment should not require reading dense terms and conditions documents. These should be front and center in the user experience — clear, plainly worded, and impossible to miss.

For users who engage with their account responsibly — making timely repayments, monitoring their spending, and using the platform’s tools to stay informed — the long-term benefits extend well beyond the immediate convenience of a credit facility. A consistently positive repayment record builds a credit score that opens doors across the entire financial system: better rates on future loans, higher credit limits, and a stronger foundation for major financial decisions like home purchases or business investment.

The trends driving adoption of digital banking platforms in India are structural rather than cyclical. Smartphone penetration continues to grow. UPI transaction volumes reach new records with regularity. A younger generation of consumers has grown up expecting the kind of instant, transparent, mobile-first experience that traditional banks have struggled to deliver.

For any Indian consumer looking to take genuine control of their financial life — building credit history, earning rewards on everyday spending, managing savings and credit in one place, and doing all of it from a smartphone in minutes — exploring what modern digital banking platforms have to offer is not just worthwhile. In 2026, it may well be the most consequential financial decision they make all year.

© 2025 Crivva - Hosted by Airy Hosting Managed Website Hosting.