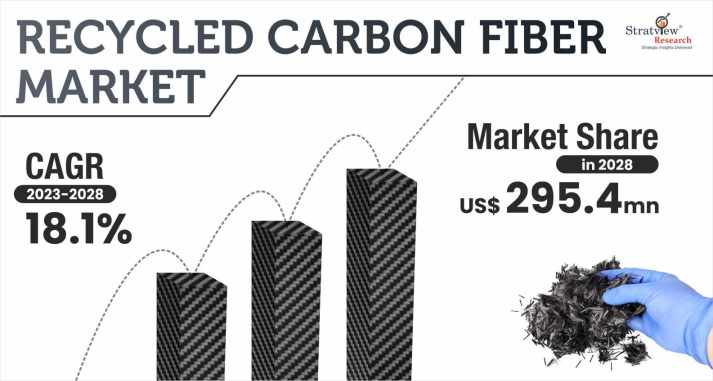

The Recycled Carbon Fiber Market was estimated at USD 104 million in 2022 and is likely to reach USD 295.4 million in 2028. The market is expected to grow at a CAGR of 18.1% during 2023-2028.

Demand acceleration is closely tied to the need for high-performance yet economical alternatives to virgin carbon fiber. Automotive OEMs are increasingly integrating recycled materials into structural and non-structural components. Assessing Recycled Carbon Fiber Market growth reveals how advancements in recycling processes and improved fiber recovery rates are enhancing product quality, making recycled carbon fiber viable for broader industrial applications.

Recycling carbon fiber refers to the process of reusing or reclaiming carbon fibers from manufacturing scraps, products, or structures that are no longer in use or have reached the end of their life cycle. The market is being supported by the rising demand for carbon fiber, the resource-intensive nature of virgin carbon fiber manufacturing, and the growing appeal of lower-cost alternatives created through recycling.

“The Recycled Carbon Fiber Market is expected to grow at a CAGR of 18.1% during 2023-2028.”

The structural basis for this growth is clear in the source: environmental concerns, resource efficiency, regulations on waste management and carbon emissions, and economic incentives are increasing the relevance of carbon fiber recycling across industries.

Request a free sample report: https://www.stratviewresearch.com/Request-Sample/953/recycled-carbon-fiber-market.html#form

Market Segmentation Analysis

The market is segmented by Form Type (Milled Fiber, Chopped Fiber, and Nonwoven), by Source Type (Aerospace Scrap, Automotive Scrap, and Other Scraps), by Waste Form Type (Dry Fiber, Textiles, Prepreg, and Composite), by End-Use Industry Type (Automotive & Transportation, Consumer Goods, Sporting Goods, and Others), and by Region (North America, Europe, Asia-Pacific, and Rest of the World).

By Form Type, the source identifies Chopped carbon fiber as the dominant type during the forecast period. The reason stated is its use in a wide variety of applications, including composites, along with its suitability for compounding processes and industrial mixing such as injection molding. The source also notes that chopped carbon fiber is less expensive than milled carbon fiber, easier to process, usable across a wider set of products, and supported by good mechanical properties. The strategic implication is that formats with broader process compatibility and lower cost are better positioned to capture recurring demand.

By Source Type, Aerospace scrap is anticipated to remain the biggest source of carbon fiber scraps during the forecast period. The source connects this directly to the aerospace industry’s reliance on carbon fiber composites for lightweight strength, fuel efficiency, and performance. It also points out that newer aircraft contain a considerable amount of carbon fiber composite content, while retirements, damage events, and strict safety and regulatory standards create a consistent stream of recyclable materials. That makes aerospace scrap structurally important to feedstock availability in this market.

By Waste Form Type, Prepreg is expected to remain the dominant waste form in the market during the forecast period. The source explains that prepregs contain a controlled and consistent fiber orientation, which makes carbon fiber separation and recovery easier during recycling. It further states that prepregs are typically free from contaminants such as paint and adhesives, which improves recycling efficiency and supports higher-quality recycled carbon fibers. Strategically, cleaner and more recoverable waste streams improve both process efficiency and output quality.

By End-Use Industry Type, Automotive & Transportation is likely to be the biggest user of recycled carbon fiber during the forecast period. The source ties this directly to applications in automotive interiors and exterior parts such as engine covers, anti-corrosion covers, front and rear bumpers, roofs, and structural parts. It also states that growing demand for lightweight vehicles, combined with the cost-effective nature of recycled carbon fiber compared with virgin carbon fiber, is expected to fuel demand. In practical terms, cost and weight reduction remain central adoption drivers in this end-use segment.

Regional Market Insights

Europe is projected to maintain its position as the biggest market for recycled carbon fibers during the forecast period. The source attributes this to the presence of major players involved in carbon fiber recycling in the region, including Procotex Corporation, Gen 2 Carbon Limited, Fairmat, and Alpha Recyclage Composites. It also states that the region benefits from major automotive OEMs, increasing demand from the automotive industry, a strong circular economy focus, and thriving automotive and aerospace industries committed to lightweight and sustainability.

Europe is also estimated to remain the fastest-growing market for recycled carbon fibers in the foreseeable future. The source links this growth to advancements in composite technology solutions and increasing penetration of composites in automotive & transportation, consumer goods, sporting goods, aerospace & defense, construction & infrastructure, and wind energy. This indicates that the region combines supply-side capability with expanding downstream use cases.

Emerging Trends Shaping the Recycled Carbon Fiber Market

The source points to a market direction shaped by more advanced and mature recycling processes. It states that industry stakeholders are working on the development of improved recycling processes and references product development activity in 2023 involving innovative technology for recycling carbon fiber plastic compounds.

Another visible direction is the deeper integration of recycled carbon fiber into industries already prioritizing lightweight materials and sustainability. The market’s segment structure and regional analysis show that adoption is being reinforced where composites usage, circular economy priorities, and cost discipline are already present. This keeps the market’s industry outlook closely tied to structural materials substitution rather than short-term shifts.

Key Growth Drivers of the Market

Competitive Landscape

Top Companies in the Market

Conclusion and Strategic Outlook

The Recycled Carbon Fiber Market was estimated at USD 104 million in 2022 and is likely to reach USD 295.4 million in 2028 at a CAGR of 18.1% during 2023-2028. The source positions this growth around environmental concerns, resource preservation, regulations, and economic incentives.

Segment data also shows a clear operating logic in the market. Chopped carbon fiber leads by form type, aerospace scrap leads by source type, prepreg leads by waste form type, Automotive & Transportation leads by end-use industry type, and Europe remains both the dominant and fastest-growing region. Together, these factors indicate a market forecast shaped by usable waste streams, process efficiency, and demand from lightweight applications.

FAQs – Recycled Carbon Fiber Market

The Recycled Carbon Fiber Market was estimated at USD 104 million in 2022 and is likely to reach USD 295.4 million in 2028. The source states that the market will grow at a CAGR of 18.1% during 2023-2028.

The source identifies escalating demand for carbon fiber, resource preservation needs, regulations on waste management and carbon emissions, and economic incentives as core growth drivers. Together, these factors make recycling a more attractive route for material supply and cost management.

Europe is projected to remain the biggest market for recycled carbon fibers. The same source also states that Europe is expected to remain the fastest-growing market in the foreseeable future.

A positive investment outlook through its growth profile, segment depth, and industry usage spread. The strongest support comes from the forecast to USD 295.4 million by 2028 and the role of industries that value lightweight, sustainability, and cost-effective alternatives to virgin carbon fiber.

© 2025 Crivva - Hosted by Airy Hosting Managed Website Hosting.