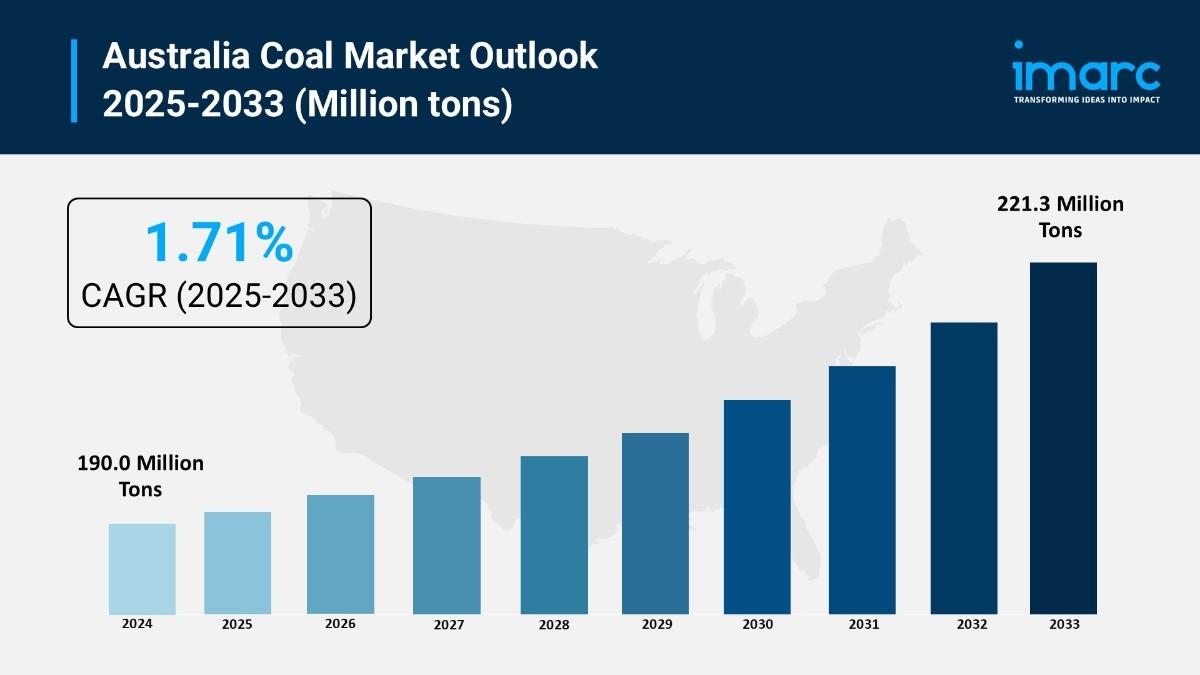

The latest report by IMARC Group, “Australia Coal Market Report by Type (Bituminous Coal, Sub-Bituminous Coal, Lignite Coal, Anthracite Coal), Mining Technology (Surface Mining, Underground Mining), End Use Industry (Power Generation, Steel, Cement, Residential and Commercial, and Others), and Region 2025-2033,” provides an in-depth analysis of the Australia coal market. The report also includes competitor and regional analysis, along with a breakdown of segments within the industry. The Australia coal market size reached 190.0 Million Tons in 2024 and is projected to grow to 221.3 Million Tons by 2033, exhibiting a growth rate of 1.71% during the forecast period.

Report Attributes and Key Statistics:

Australia Coal Market Overview:

The Australia coal market is driven by competitive mining labor costs, stable domestic demand for coal-based energy, expanding export capacity at Australian ports, and continual technological advancements in coal mining. Australia second-largest thermal coal exporter after Indonesia with nation exported 209 million tonnes coal 2024. Coal export earnings projected AUD 32 billion year ending June 2025. Australia holds world’s largest economic resources iron ore gold lithium bauxite nickel uranium playing pivotal role global energy transition. December 2024 four coal mine approvals Caval Ridge Boggabri Lake Vermont Vulcan South announced hot on heels three expansion projects Hunter Valley September 2024. Queensland Bowen Basin among world most lucrative sources coking coal supporting sustained nationwide market expansion.

Request For Sample Report: https://www.imarcgroup.com/australia-coal-market/requestsample

Australia Coal Market Trends:

Market trends indicate slow transition away from thermal toward metallurgical coal exports with rising environmental regulations growing demand emerging Asian economies. Rising demand bituminous coal especially from developing nations valued high energy content flexibility fuel choice power production industrial applications. Investment going into cleaner technology automation with domestic usage decreasing. Premium-grade coal production trade diversification driving industry changing strategic direction. Technology improvements remote operations especially large coalfields Galilee Surat Basins improving cost-effectiveness operational efficiency. Coal power although diminishing urban areas remains main source energy regional outer communities where alternatives less feasible supporting market maturation transformation nationwide.

Australia Coal Market Drivers:

Drivers include availability resources strategic geographical location with rich natural resource high-grade thermal metallurgical coal particularly Queensland New South Wales. Queensland Bowen Basin among world most lucrative sources coking coal with abundant resources low extraction costs open-cut mining methods. Located near industrially fast-growing economies Asia China India South Korea Japan enjoying shorter transportation time distance compared other major coal exporting countries. Export-oriented policy framework trade relations with federal state authorities promoting mining global trade streamlining approvals new coal mines infrastructure. Strong bilateral trade ties Free Trade Agreements with South Korea Japan reducing tariff barriers facilitating trade logistics. Industrial demand regional economic dependency with metallurgical coal supporting steel manufacturing essential infrastructure construction. Economic embeddedness guaranteeing broad national energy export policy support sustained market growth nationwide expansion.

Market Challenges:

Market Opportunities:

Australia Coal Market Segmentation:

By Type:

By Mining Technology:

By End Use Industry:

By Regional Distribution:

Australia Coal Market News:

September 2025: BHP suspended operations Saraji South resulting 750 job cuts citing high state government royalties as key factor behind decision. Company financial position Queensland reflecting broader industry challenges where effective tax burdens reached levels questioning long-term viability coal operations. Queensland escalating royalty structure emerged primary catalyst forcing BHP reassess coal portfolio creating unsustainable fiscal environment metallurgical coal producers supporting industry restructuring nationwide.

August 2025: Bravus Mining and Resources announced substantial capital investment increase production Carmichael mine near Clermont central Queensland. Investment demonstrating continued confidence coal sector despite climate concerns environmental pressures. Carmichael mine expansion highlighting industry determination expand leveraging Queensland Bowen Basin lucrative coking coal resources supporting regional employment economic development nationwide.

Key Highlights of the Report:

Frequently Asked Questions (FAQs):

Q1: What are the primary factors driving Australia coal market growth to 221.3 million tons by 2033?

A1: Market driven by availability resources strategic geographical location Queensland Bowen Basin lucrative coking coal sources, export-oriented policy framework Free Trade Agreements reducing tariff barriers, industrial demand metallurgical coal supporting steel manufacturing infrastructure, coal export earnings projected AUD 32 billion year ending June 2025 nation exported 209 million tonnes 2024, December 2024 government approved four extensions Hunter Valley projects supporting 1.71% CAGR nationwide.

Q2: How are royalty pressures and export diversification transforming Australia coal landscape?

A2: September 2025 BHP suspended operations Saraji South 750 job cuts citing high state government royalties Queensland escalating royalty structure creating unsustainable fiscal environment metallurgical coal producers. Industry facing declining exports despite government forecasting growth with Australia actual metallurgical coal exports declining last five years. Export market diversification targeting India Southeast Asia markets growing industrial demand. Premium-grade coal production trade diversification driving industry strategic direction supporting transformation nationwide.

Q3: What opportunities exist for coal stakeholders in emerging Australia market segments?

A3: Opportunities include metallurgical coal focus capitalizing sustained demand steel production requirements, export market diversification targeting India Southeast Asia growing industrial demand, premium quality products leveraging Australian coal lower ash sulphur competitive advantage, technology integration deploying automation remote monitoring improving productivity, infrastructure expansion government financing mining railways ports, carbon capture storage implementing cleaner technology, regional development government programs workforce training, and strategic partnerships forming alliances international buyers securing long-term contracts supporting nationwide expansion.

Note: If you require specific information not currently within the scope of the report, we can provide it as part of the customization.

Ask an analyst for your customized sample: https://www.imarcgroup.com/request?type=report&id=24687&flag=C

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services. IMARC offerings include market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel. No.: (D) +91 120 433 0800

Americas: +1 201-971-6302

© 2025 Crivva - Hosted by Airy Hosting Managed Website Hosting.