Market Overview:

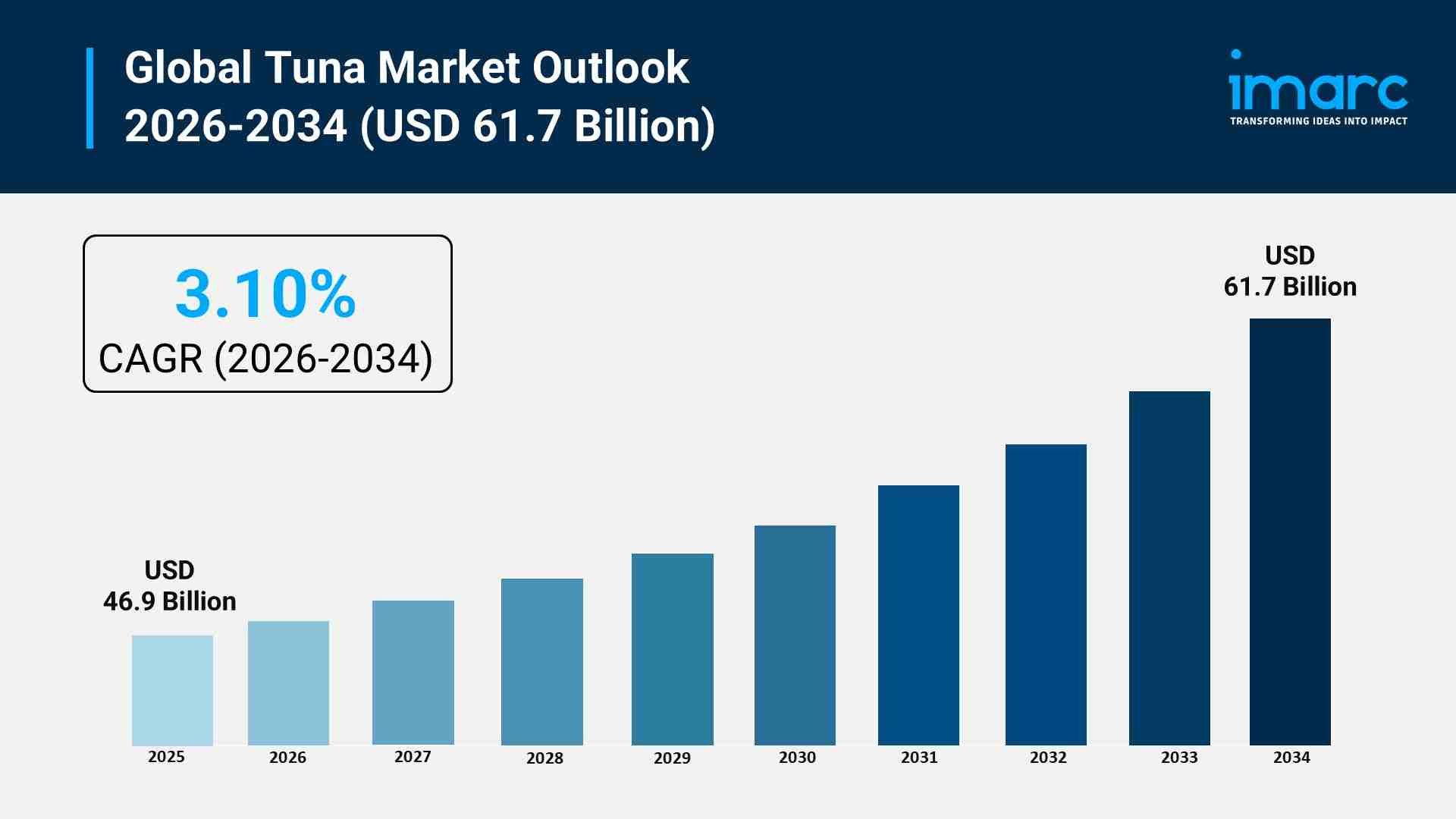

The tuna market is experiencing rapid growth, driven by surging consumer demand for nutrient-dense proteins, innovations in processing and cold chain logistics, and proliferation of ready-to-eat and convenience formats. According to IMARC Group’s latest research publication, “Tuna Market Size, Share, Trends and Forecast by Species, Type, and Region, 2026-2034“, The global tuna market size was valued at USD 46.9 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 61.7 Billion by 2034, exhibiting a CAGR of 3.10% during 2026-2034.

This detailed analysis primarily encompasses industry size, business trends, market share, key growth factors, and regional forecasts. The report offers a comprehensive overview and integrates research findings, market assessments, and data from different sources. It also includes pivotal market dynamics like drivers and challenges, while also highlighting growth opportunities, financial insights, technological improvements, emerging trends, and innovations. Besides this, the report provides regional market evaluation, along with a competitive landscape analysis.

Download a sample PDF of this report: https://www.imarcgroup.com/tuna-market/requestsample

Our report includes:

The global appetite for healthy, high-protein diets is a primary engine for the tuna industry, as consumers increasingly prioritize lean meats rich in omega-3 fatty acids. This shift is particularly evident in the United States, where the National Fisheries Institute identifies canned tuna as the third most popular seafood item, and in Japan, the world’s largest consumer. In the United States, the Food and Drug Administration (FDA) categorizes canned light tuna as a “Best Choice” for nutrition, recommending up to three servings per week to support heart and brain health. This official health endorsement has catalyzed a resurgence in household penetration. Furthermore, the World Bank notes that per capita fish consumption increased by 40% between 1990 and 2023, with tuna maintaining its status as a central pillar of the high-protein market. As middle-income households in urban regions prioritize wellness, the demand for tuna as a functional food continues to strengthen across both developed and emerging economies.

Technological advancements in seafood preservation are significantly expanding the reach and quality of tuna products. Modern processing techniques, such as high-pressure processing (HPP) and cryogenic freezing innovations showcased by companies like Linde, allow tuna to retain its flavor and nutritional profile without the need for chemical additives. These methods extend shelf life and improve the safety of raw-consumption products, which is vital for the expanding sushi and sashimi sectors. Additionally, the Food and Agriculture Organization (FAO) reports that nearly 50% of fish processing costs are tied to cold chain logistics, prompting industry leaders to invest in energy-efficient cold storage and vacuum-sealing technologies. In South Korea, Dongwon Group has leveraged its integrated logistics and purse seiner operations to optimize these supply chains. Such infrastructure improvements enable the efficient export of high-value frozen tuna from the Western and Central Pacific—which accounts for nearly 60% of the global catch—to distant markets in Europe and North America.

The rapid pace of modern urban life is driving a massive transition toward convenient, shelf-stable, and ready-to-eat (RTE) tuna products. Canned and pouch-packaged tuna currently dominate the market, with the canned segment alone holding a share of over 66% in 2025. Major industry players like Thai Union and its brand John West are leading this growth by launching nutrient-rich, flavored ranges specifically designed for on-the-go consumption. For instance, Frime S.A.U. recently introduced a unique “ready-to-eat” marinated tuna segment suitable for raw consumption, catering to the growing “poke bowl” trend. In Asia-Pacific, rising disposable incomes and the adoption of Western-style convenience diets have seen processed tuna imports in Japan rise from 65,000 tons in 2018 to 69,000 tons in 2022. These value-added formats, which include spicy, lemon-pepper, and herb-infused varieties, reduce meal preparation time and appeal to a younger demographic seeking nutritious alternatives to traditional fast food, thereby solidifying tuna’s presence in the global retail sector.

A transformative shift is occurring as the industry moves from traditional “ranching”—which relies on catching wild juveniles—toward full-cycle aquaculture. This trend is driven by the commercialization of closed-cycle hatchery technology, particularly in the Mediterranean and Asia-Pacific. In 2025, the Asia-Pacific region contributed 43% of the farmed tuna market, while countries like Turkey and the United Arab Emirates are scaling offshore cages to stabilize supply. This evolution is crucial because tuna typically require 15 to 20 kilograms of forage fish to gain just one kilogram of weight, making feed efficiency a major focus. By developing closed-cycle systems, companies can reduce their dependence on wild stocks and mitigate the impact of price volatility in forage fish like anchovies. Governments are also backing this shift; for example, Saudi Arabia’s Vision 2030 has allocated $500 million toward offshore cage projects to enhance food security and reduce the environmental footprint of traditional fishing.

Transparency is no longer optional in the tuna market, as brands adopt sophisticated digital tools to prove the legality and sustainability of their products. The implementation of Electronic Bluefin Catch Documents (e-BCD) and Electronic Catch Documentation Schemes (e-CDS) has become mandatory in major importing blocs to combat illegal, unreported, and unregulated (IUU) fishing. Furthermore, the International Seafood Sustainability Foundation (ISSF) is advocating for the broad implementation of electronic monitoring (EM) on vessels, using AI-powered cameras and GPS trackers to replace or assist human observers. This trend allows consumers to scan QR codes on products to trace a specific tin of tuna back to the vessel and the ocean region where it was caught. This high level of accountability is essential for maintaining Marine Stewardship Council (MSC) certifications, which now cover a significant portion of the skipjack and yellowfin stocks in the Western and Central Pacific Ocean.

The “green” revolution in packaging is fundamentally changing how tuna is presented on retail shelves. Beyond the fish itself, consumers are demanding that the containers be as sustainable as the sourcing. This has led to a surge in the use of BPA-free cans, recyclable pouches, and biodegradable materials, with global demand for eco-friendly packaging materials increasing by 1.2 million metric tons in 2022. Companies are also focusing on reducing water usage and carbon footprints during the canning process; for instance, a leading producer recently implemented an automated canning system that achieved a 15% increase in production efficiency and a 10% reduction in water consumption. This trend toward “clean” packaging complements the move toward organic and sustainably caught products. As environmental regulations tighten, particularly in the European Union, which accounts for over 26% of global tuna consumption, brands that prioritize plastic-free and low-impact packaging are gaining a significant competitive advantage.

We explore the factors propelling the global tuna market growth, including technological advancements, consumer behaviors, and regulatory changes.

Leading Companies Operating in the Global Tuna Market Industry:

Tuna Market Report Segmentation:

By Species:

Skipjack dominates the market with 57.8% share in 2024 due to abundant supply, eco-friendliness, and versatility in food preparation.

By Type:

Canned leads the segment with 70.9% market share in 2024, favored for its convenience, affordability, and widespread availability.

Production Analysis by Region:

Indonesia holds the largest market share at 9.4% in 2024, benefiting from vast maritime resources, sustainable practices, and government support.

Regional Insights:

European union accounts for 26.8% of the market share in 2024, driven by high seafood demand, strong processing industries, and established trade networks.

Note: If you require specific details, data, or insights that are not currently included in the scope of this report, we are happy to accommodate your request. As part of our customization service, we will gather and provide the additional information you need, tailored to your specific requirements. Please let us know your exact needs, and we will ensure the report is updated accordingly to meet your expectations.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91-120-433-0800

United States: +1-201-971-6302

© 2025 Crivva - Hosted by Airy Hosting Managed Website Hosting.