Australia Vehicle Financing Market Overview

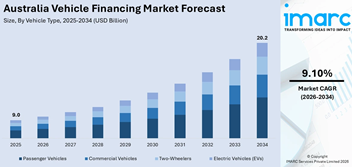

The australia vehicle financing market size reached USD 9.0 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 20.2 Billion by 2034, exhibiting a growth rate (CAGR) of 9.10% during 2026-2034.

Vehicle financing encompasses the range of financial products and services that enable consumers and businesses to acquire motor vehicles through structured credit arrangements rather than outright cash purchases. These products include secured auto loans, chattel mortgages, finance leases, novated leases, hire purchase agreements, guaranteed future value (GFV) loans, and emerging subscription and pay-per-use models. In Australia, vehicle financing is a critical enabler of automotive market activity, with the majority of new and used vehicle acquisitions funded through some form of credit facility. The financing ecosystem involves banks, credit unions, non-bank lenders, fintech platforms, original equipment manufacturer (OEM) captive finance companies, and broker networks that collectively provide consumers and fleet operators with diverse options tailored to their credit profiles, tax circumstances, and ownership preferences

Artificial intelligence is fundamentally transforming the Australian vehicle financing market, enabling lenders to deliver faster approvals, more accurate credit assessments, personalized product offerings, and enhanced fraud detection while dramatically reducing operational costs. AI-driven credit scoring and biometric authentication are becoming increasingly popular among digitally empowered consumers, particularly younger demographics who expect instant, seamless financial services. Key areas where AI is reshaping the market include:

Request for a sample copy of this report: https://www.imarcgroup.com/australia-vehicle-financing-market/requestsample

Electric Vehicle Financing Innovation and Green Lending Products

One of the most significant trends shaping the Australian vehicle financing market is the emergence of specialized financing products designed to accelerate electric vehicle adoption. As EV penetration surges—driven by government fringe benefit tax exemptions for zero-emission vehicles, declining battery costs, and expanding charging infrastructure—lenders are developing tailored finance solutions that address the unique economics of electric vehicle ownership. Guaranteed future value (GFV) loans have gained substantial traction for EV purchases, as they mitigate consumer concerns about rapid battery depreciation by guaranteeing a minimum residual value at the end of the loan term. CommBank’s reported 161% increase in EV finance demand reflects the broader industry trend, with major banks and fintech platforms competing to capture the growing EV lending segment through discounted green loan rates, extended loan terms that align with longer EV lifespans, and integrated charging infrastructure financing packages. Novated lease arrangements have become particularly popular for EV acquisitions, as the salary sacrifice structure combined with the FBT exemption creates compelling total-cost-of-ownership advantages. OEM captive finance arms—including those operated by Tesla, BYD, and legacy manufacturers transitioning to electric—are offering competitive factory-backed financing that bundles vehicle purchase, warranty, and charging solutions. This trend is creating a distinct green vehicle financing vertical that is growing significantly faster than conventional auto lending and attracting new specialist lenders to the market.

Digital-First Lending and Open Banking Transformation

The Australian vehicle financing market is undergoing a rapid digital transformation, with fintech platforms and digitally progressive traditional lenders reshaping the borrower experience through end-to-end online journeys, open-banking-enabled assessments, and real-time settlement capabilities. The Consumer Data Right (CDR) framework, which enables open banking in Australia, is allowing lenders to access applicants’ financial data—with consent—directly from their bank accounts, replacing manual income verification and bank statement collection with instant, accurate financial assessments that accelerate approval decisions. Fintech lenders such as Plenti have expanded their vehicle finance platforms with AI-powered pre-approval capabilities and NAB PayTo integration for instant repayments, demonstrating the competitive advantages of technology-led lending models. Traditional banks are responding with their own digital upgrades, embedding vehicle finance applications within mobile banking apps and creating seamless pathways from vehicle search to finance approval. The digitization trend is extending to the broker channel, where digital platforms are enabling finance brokers to submit applications, compare multiple lender offers, and manage settlements electronically, reducing processing times and improving customer transparency. For consumers, digital-first lending delivers convenience through anytime-anywhere access, faster decision-making, and reduced documentation burden, while for lenders it reduces origination costs, improves data quality, and enables real-time portfolio monitoring that enhances credit risk management.

Rising Vehicle Prices and Increasing Average Loan Values

The sustained increase in average vehicle transaction prices across both new and used segments is serving as a fundamental growth driver for the Australian vehicle financing market. New vehicle prices have risen significantly due to the growing consumer preference for SUVs, utes, and premium models that command higher price points, the inclusion of advanced safety and technology features as standard equipment, and the premium pricing of electric and hybrid vehicles compared to equivalent internal combustion engine models. Used vehicle prices, while moderating from pandemic-era peaks, remain elevated compared to historical norms due to constrained new vehicle supply chains and strong residual demand. These higher price points directly increase the average loan size originated, expanding the total value of the vehicle financing market even when unit volumes remain stable. The higher capital outlay required for vehicle purchases is also increasing consumer reliance on financing—a larger proportion of buyers who might previously have purchased outright are now utilizing credit facilities to manage cash flow. For lenders, higher average loan values improve revenue per origination while maintaining similar processing costs, enhancing unit economics across the lending portfolio. The premiumization trend in the Australian automotive market, combined with the higher upfront costs of EV acquisition, ensures that average loan values will continue their upward trajectory, structurally supporting financing market growth.

The market has been segmented based on the following criteria:

Breakup by Finance Type:

Breakup by Vehicle Condition:

Breakup by Provider Type:

Breakup by Region:

Note: If you require any specific information not currently covered within the scope of the report, IMARC Group will provide it as part of customization.

Speak to an analyst

𝗔𝗯𝗼𝘂𝘁 𝗨𝘀

IMARC Group is a global management consulting firm that helps companies in strategy formulation, finding the right audience for their products, and sourcing the best talent. We have been in the industry since 2014 and have helped over 1,000 companies worldwide. We provide market research, competitive analysis, and market intelligence services to help companies in various industries achieve their goals.

𝗖𝗼𝗻𝘁𝗮𝗰𝘁 𝗨𝘀

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No: (D) +91 120 433 0800

United States: +1-631-791-1145

© 2025 Crivva - Hosted by Airy Hosting Managed Website Hosting.